It’s difficult to sum up 2013 from a climate standpoint, other than to note that it was a year of contrast and just a little irony. Overall progress in actually dealing with the issue of global emissions made some minor gains, although there were a few setbacks of note along the way as well.

- The IPCC released the climate science part of their 5th Assessment Report and that managed to keep the media interested for about a day, after which it was back to issues such as health care, economic growth, Euro-problems and assorted regional conflicts. Importantly, the report introduced into the mainstream the much more challenging model for global emissions, which recognizes that it is the long term accumulation that is important, rather than emissions in any particular year.

- The global surface temperature trend remained stubbornly flat, despite every indication that the heat imbalance due to increasing amounts of CO2 in the atmosphere remains in place and therefore warming the atmosphere / ice / ocean system somewhere, although where exactly remained unclear. The lack of a clear short term trend became a key piece of evidence for those that argue there is no issue with changing the concentration of key components of the atmosphere, which further challenged the climate science community to provide some answers.

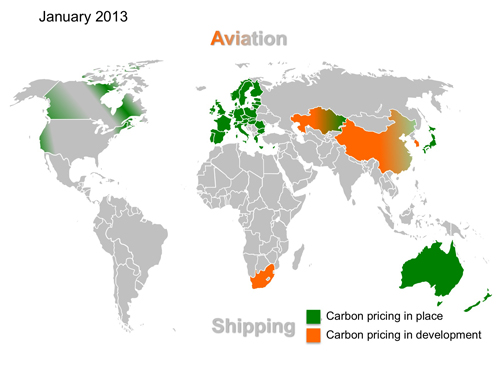

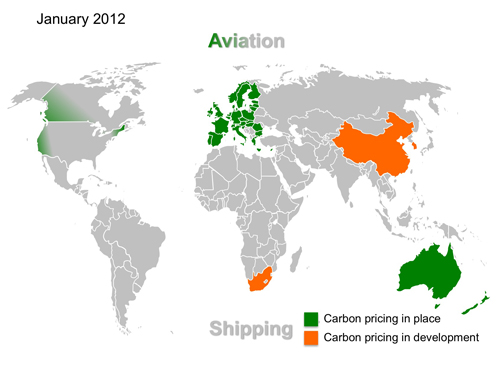

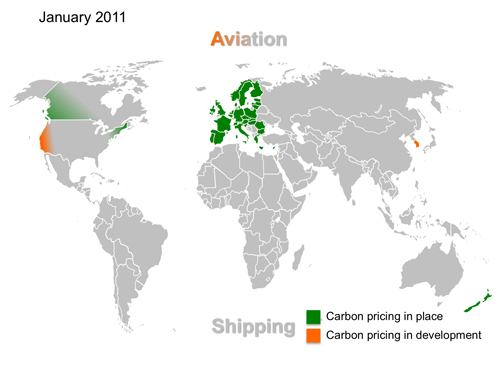

- The UNFCCC continued to put a brave face on negotiations that are being seriously challenged for pace by most of the worlds declining glaciers while the world’s largest emitter, China, often thought of as blocking progress at the international level kicked off a number of carbon pricing trial systems in various parts of the country.

- Australia elected a government that proudly announced on its first day in office that the carbon pricing system which was finally in place and operating after eight years of arguing would be dismantled, only to be confronted by the fact that the country sweltered under the hottest annual conditions ever recorded in that part of the world.

- Several very unusual global weather extremes were reported, including what may be the most powerful ever storm to make landfall, yet there was a distinct lack of desire by scientists and commentators to attribute anything to the rising level of CO2 emissions in the atmosphere, except perhaps for the UNFCCC negotiator from the Philippines who went on a brief hunger strike in response to devastation that hit parts of his country.

- The EU carbon price remained in the doldrums for the entire year, although did show a few signs of life as the Commission, Parliament and various Member States teased, tempted and taunted us with the prospect of action to correct the ETS and set it back on track. In the end, the “backloading” proposal was passed by the Parliament and will likely be adopted and implemented, but the test will be whether or not the Commission now has the backbone to propose and unconditionally support the necessary long term measures to see the ETS through to 2030 as the main driver of change.

- For the first time that I had seen, a book was released that finally got to grips with the emissions issue, yet somewhat alarmingly failed to find any clear route out of the dilemma we collectively find ourselves in. “The Burning Question”, by Mike Berners-Lee and Duncan Clarke recognized how difficult the emissions challenge has become and questioned those who trivialize the issue by arguing that more renewable energy and better efficiency is all that is needed to solve the problem. Clearly a book for those who designed the hallway posters [Link] at COP19 in Warsaw to read. Closer to home, new Shell Scenarios released in March [Link] 2013 did chart a pathway out of the emissions corner that Mike and Duncan painted themselves into, but the much discussed 2°C wasn’t quite at the end of it.

- The IEA put climate change back in the headlines of their World Energy Outlook, with a special supplement released in June outlining a number of critical steps that need to be taken to keep the 2°C door open. Unfortunately they hadn’t taken the time to read “The Burning Question” and consequently positioned enhanced energy efficiency as a key step to take over this decade.

- In North America both the US and Canadian Federal governments continued to head towards a regulatory approach to managing emissions, while States and Provinces respectively continued to push for carbon pricing mechanisms. California and Quebec linked their cap and trade systems to create a first cross border link in the region.

- The World Bank Partnership for Market Readiness continued its mission of preparing countries for carbon markets and carbon pricing, with numerous “works in progress” to show for the efforts put in to date. But the switch from early trials and learning by doing phases to robust carbon trading platforms underpinning vibrant markets remains elusive.

These were all important steps, particularly those that tried to broaden or strengthen the role of carbon pricing. On that particular issue, 2013 saw both positive and negative developments, with progress best described as “baby steps” rather than anything substantial. With a change in the European Parliament, mid-term elections in the US and Australia in the process of unwinding, it is difficult to see where the big carbon pricing story in 2014 will come from. Perhaps the tinges of orange (see below) now beginning to appear in South America will flourish and green with COP20 being held in that region towards the end of the year.

Perhaps it should be considered a “pause”, or a “hiatus”. Perhaps that “pause” or “hiatus” will continue in 2014.

Ed,

You might find this Nature paper, The Case of the Missing Heat, to be quite interesting.

David