If carbon dioxide emissions are to fall by 50% by 2030, i.e. to 20 Gt, then what might that look like? In just a decade the global energy system would need to look very different.

David Hone – Chief Climate Change Advisor for Shell

If carbon dioxide emissions are to fall by 50% by 2030, i.e. to 20 Gt, then what might that look like? In just a decade the global energy system would need to look very different.

China has set the goal of being carbon neutral by 2060. What might the transition look like and what has to happen in the 2020s to get started?

As the EU works to reset its emission reduction goals to align more closely with the 1.5°C goal of the Paris Agreement, a question arises around the scale and scope of the energy transition required. What will it look like? How fast should it proceed? Which technologies need to be accelerated to achieve the desired outcome? To help answer these and provide a perspective on the transition, my colleagues in the Shell Scenario team have produced a scenario sketch of the journey forward, arriving in 2050 with a net-zero emissions energy system (NB: The pathway was formulated in late 2019 prior to the COVID-19 pandemic and therefore does not include the energy system disruption being seen in 2020).

From a policy perspective, the EU has been addressing the climate issue for at least 15 years, with the EU Emissions Trading System in place since 2005. The 2020 energy situation arises from the 2007 climate and energy package, which included three key targets:

The targets were set by EU leaders in 2007 and enacted in legislation in 2009. They are also headline targets of the Europe 2020 strategy for smart, sustainable and inclusive growth. Within this, the EU Emissions Trading System is the EU’s key tool for cutting greenhouse gas emissions from large-scale facilities in the power and industry sectors, as well as the aviation sector. The ETS covers around 45% of the EU’s greenhouse gas emissions. In 2020, the target is for the emissions from these sectors to be 21% lower than in 2005.

The year 2020 represents a halfway point from 1990 to 2050, during which 20% of the hard deployment work has been done, but with a number of key technologies available at scale that hardly existed or didn’t exist around the turn of the century. Solar PV and Electric Vehicles are two examples (although solar PV did exist in 2000, it was expensive and small scale). That leaves just 30 years for the remaining 80% reduction, which must also include bringing to scale several other technologies which are yet to be deployed in the EU. This is a tall order and the scenario sketch illustrates how extraordinarily stretching it will be.

The additional key technologies that must move quickly to scaled deployment are as follows;

On the assumption that development and demonstration of all the above proceeds rapidly, deployment kicks in for most during the 2030s. But in the 2020s the energy technologies that have been nurtured over the last twenty years must be accelerated. For example, by 2030 solar must be quadruple current deployment, wind nearly triple current deployment and nuclear must be growing again, not declining.

In the 2030s the really hard work starts, with carbon capture and storage moving from first demonstration in the EU by 2025 to 40 medium sized facilities (one million tonnes CO2 stored per annum) by 2030 and over 100 by 2035. New technologies such as hydrogen fuel cell trucks must become ubiquitous during the 2030s, with at least 600,000 vehicles on the road by the end of that decade.

All of the above will require both technology development incentives and deployment policies. The analysis assumes a rising carbon pricing mechanism – whether explicit or implicit – to more than €200 per tonne of CO2 equivalent by 2050 to deliver and sustain the emission cuts and CO2 management necessary for the EU to reach climate neutrality. But even the EU ETS will need to change, as I discussed in a recent post.

While carbon pricing is an efficient lever for reallocating resources and driving behavioural change, it will not be enough on its own. A sectoral approach to policy which brings clean technologies, fuels and products to market, as well as their deployment and diffusion at scale, must urgently be developed. It is essential that policy should help provide consumers and businesses with low-carbon alternatives to adopt.

In the sketch, 2050 marks a point of climate neutrality for Europe, helped by the development of large scale carbon sinks through reforestation. But this isn’t the end of the transition, merely a point of significance. The hydrogen economy will continue to grow, electrification of industry will expand and efficiency gains will continue to be made. As was illustrated in the Sky Scenario, Europe will likely shift to become a net-negative emission economy during the second half of the century, a necessary requirement to ensure global net zero emissions and a 1.5°C limit on warming.

Download the EU Sketch here.

Last week the Climate Change Committee (CCC) in the UK released its much anticipated report which is recommending that the government revise its emissions goal to net-zero in 2050. The Committee notes that this is an appropriate UK contribution towards the global need of meeting the goals of the Paris Agreement. The recommendation also follows in the wake of the IPCC Special Report on 1.5°C, which identified 2050 as the year in which the global economy should attempt to reach net-zero emissions in order to limit warming to 1.5°C with a 66% probability.

The recommendation is a shift from the current UK target which would see the country reach an 80% reduction by 2050, in support of which the country is broadly on track to deliver the first 3 interim carbon budgets to 2022. However, as it looks past 2022 the CCC notes there is insufficient early development of some technologies for the heavy lifting ahead. Examples of this include carbon capture and storage (CCS) and hydrogen for a variety of uses.

Nevertheless, the state of technology development, deployment and availability has shifted since the time of the first UK target back in 2008. The cost of wind and solar has dropped significantly, offshore wind is now a viable proposition, many electric car models are available and while not in the UK, some 20 CCS facilities are now running in various parts of the world. All of the technologies required to do the job set out by the CCC are in plain sight, although a number still require significant UK development for deployment in this country. The CCC report is also very clear on this issue.

2050 is just over thirty years away and that same time period reflecting backwards marks the time that I first arrived in the UK with Shell. In the next 30 years the whole energy system will need to shift to achieve net-zero emissions, but how does that compare with the changes seen over the last 30 years. While two thirds of that period has not been covered by the Climate Change Act and its carbon budgets, all but three years have been covered by the UK ratification of the UN Framework Convention on Climate Change.

The Sankey diagrams below reflect the change over the period, although the most recent from the IEA are 2016, so they won’t show the last two years of renewable energy development.

Overall primary energy consumption has fallen, with the most visible change being the shift away from coal and towards natural gas in power generation. Both bioenergy and renewables have also added to the generation mix. Nuclear plays an important and steady base load function. Natural gas is now the dominant contributor to the current power generation sector and in the past year there have been periods where coal has not played a role at all. Back in 1989 coal made up most of the generating capacity. Oil demand within the UK has hardly changed over thirty years (slightly up) although production has halved.

As noted above, one feature that has surged since 2016 is the proportion of renewable energy in the generation mix. Recent figures from BEIS show that wind and solar have now exceeded nuclear on a quarterly basis.

In the final energy system, the changes are more nuanced. The overall share of electricity has moved from 16.7% of final energy to 20.4%, or a shift of 3.7% points in 27 years. The global rate of change is tracking at 2% points per decade, so the UK is well short of that pace of transition. A net zero emissions economy would likely need electricity to be the major component of final energy, say around 60%, so the UK rate of change will need to shift from 1.37% points per decade to around 11% points in each of the coming decades.

Transport hasn’t shifted at all in the past 30 years, with oil use in transport slightly increasing. Electricity is just starting to creep into this mix, but pure electric vehicles have reached only 0.7% (2018) of new car sales. Worryingly, the total number of petrol and diesel cars registered in the UK in 2018 was unchanged from 2013, a period which has seen the first major push to get consumers to go electric. Reaching net-zero emissions by 2050 will not just mean seeing all new purchases as electric, but seeing all new purchases from about 2035 onwards as electric. It can take up to 15 years to completely turn over the entire on-the-road fleet, although a future government could presumably accelerate this process with a buy-back-and-scrap scheme.

In the industrial sector, energy consumption has dropped by nearly a third, presumably through efficiency improvements as industrial output has hardly changed (see chart below). Importantly, electricity use has stayed largely the same. This means that the sector is gradually electrifying, although again the pace of change is below that required.

UK Industrial Production (1970-2019).

Then there are the tricky bits, where the UK has made only limited progress. The CCC notes that radical change is needed in home heating, including a shift to hydrogen and heat pumps, with support from much better home insulation. But residential natural gas use has marginally increased in 30 years, despite significant improvements in boiler efficiency and the use of electricity instead of gas for new apartment buildings. One highlight in this area is the recent milestone of one million homes now being supplied with biomethane.

The overall change in 30 years has been one of continually falling greenhouse gas emissions, with much of the gain coming from natural gas replacing coal and a fall in industrial energy use. While the impetus for change over the last 30 years was perhaps not as great as it is now, the overall shift is symptomatic of typical energy system dynamics; rapid adjustment has never been a feature, primarily due to the large capital stock involved. Outside the energy sector change over the same period has been dramatic. In 1989 there was no internet, no social media, hardly a mobile phone to be seen and televisions were defined more by their depth than their width. So can the UK reach these sorts of transition rates and achieve the goal of net-zero emissions by 2050?

In the power generation sector, zero emissions should be entirely achievable in that time frame. Renewables are surging and new nuclear capacity is now under construction (although even getting that started took a decade). Similarly, with the models on offer or on their way, passenger vehicles could be entirely electric and various cities across the UK have demonstrated that electric buses are now a viable option. But there is no real sign of change for heavy goods vehicles, shipping or aviation. Perhaps the biggest challenge sits with the use of natural gas in homes and industry. It is easy to use, clean, provides a very high heat load and is backed by extensive infrastructure. Hydrogen and electrification are potential pathways forward, but as noted the electrification rate of change has to shift by nearly an order of magnitude. For hydrogen there are promising signs of change with the government now funding a major programme on supply and conversion of existing facilities away from natural gas.

Finally, there is carbon capture and storage (CCS), which may be a simpler solution in many applications than attempting to dislodge natural gas. CCS in combination with direct air capture (still a nascent technology) may also be needed to balance out emissions in sectors such as aviation. Even the production of hydrogen may be easiest at scale from natural gas, which would then also require CCS. The UK has tried and tried again with CCS, but there is still no operational facility to show for all the efforts made. Yet the UK is both pipeline dense and geologically gifted in terms of storage potential, so deployment could proceed given the right incentives to begin.

The Climate Change Committee have put forward a bold recommendation, but it is not without immense challenge. It ought to be possible to achieve the 2050 goal of net-zero emissions, but it won’t happen without some significant nudging by the government in a number of key areas. Policy decisions over the coming five years may well set the scene for the next twenty, so there is everything to play for.

Over recent weeks and months there has been considerable discussion in the USA and Canada on clean energy transition pathways, carbon pricing and the Paris Agreement. This has been catalysed by the IPCC 1.5° report, the arrival of new political figures on the scene and the prospect of elections in 2019 and beyond. As I discussed in my recent post on a new report that outlines a pathway for global transition consistent with 1.5°C, very steep emission reductions are called for in North America over the coming decade, as shown in the chart below. For the 1.5° case, a reduction of about 80% is proposed from 2015 to 2030.

Source: Achieving the Paris Climate Agreement Goals – Sven Teske (Editor)

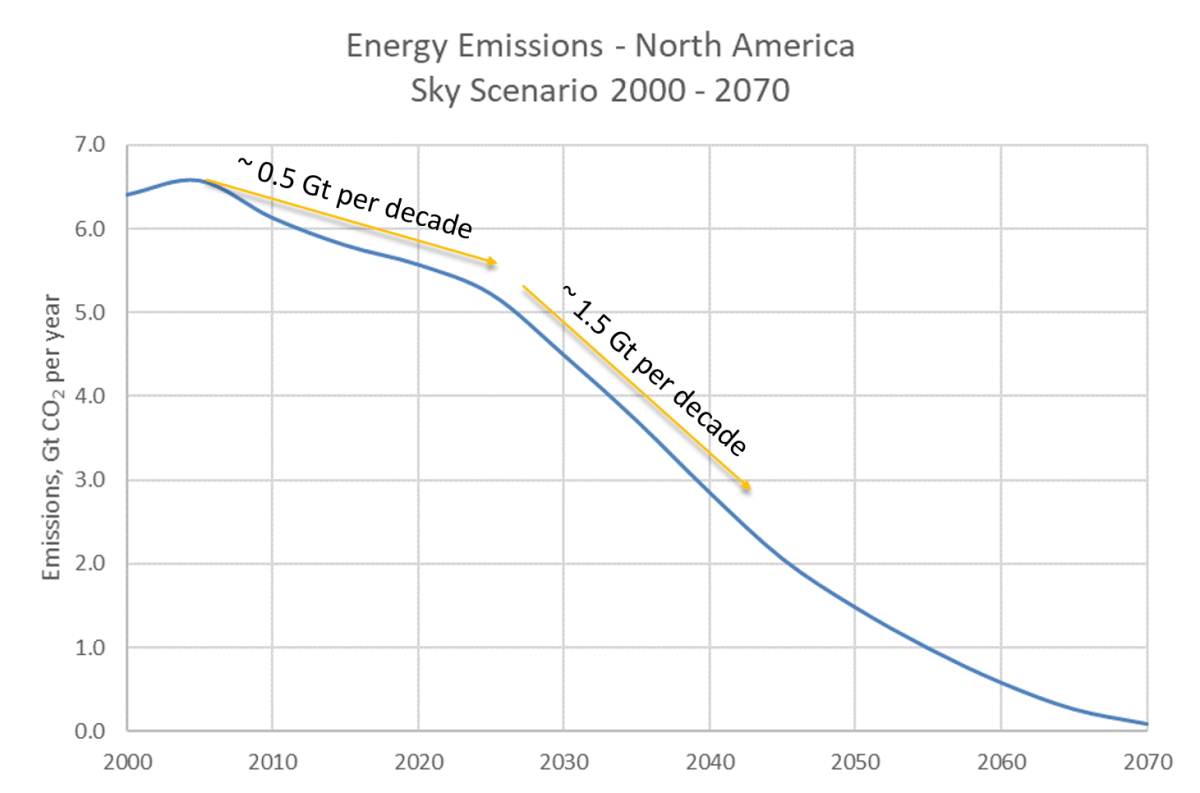

But is such a rapid transition possible for an energy system as large as that found in the USA? This is similar to a pathway that has been proposed by those calling for a Green New Deal in the USA. But it is very different to that proposed by the Sky Scenario, released by Shell in 2018.

In Sky, to reach the goals of the Paris Agreement, global emissions need to peak in the 2020s and be falling by 2030, which happens in large part through an initial mobilization of effort throughout the 2020s. But emissions in the USA don’t get even close to an 80+% reduction in that time. North American emissions peaked around 2005 and are slowly falling, but in Sky the pace of change triples in the 2020s with a significant boost in effort, led by government policies such as carbon pricing and electric vehicle mandates and incentives. But by 2030, emissions have fallen by only 23% compared with 2015.

This would constitute a major shift in direction for the US economy. Five significant changes in the energy system in the decade to 2030 in Sky for North America are;

To imagine even more than this is quite challenging. In the EV sector, sales in the USA in 2018 grew rapidly, but still only amounted to 2.1% of the total (Source: EVVolumes.com). A looming issue is the lack of EV models in the SUV / light truck category, although this should start to correct in 2020 with several expected. Nevertheless, this category size makes up a large portion of the US market and it may take some time for consumers to adopt electric versions of their favourite model. While an all EV sales line up might be possible by 2030, an all EV fleet isn’t. For a 100% EV fleet to occur in 2030, all new passenger vehicle sales need to be electric in the next year or two.

In the power generation sector, the multipliers given for wind and solar above, together with an unchanged role for nuclear, results in over half the power generation coming from non-fossil sources by 2030. In Sky, it isn’t until after 2040 before coal is phased out, but natural gas persists in the power mix until the 2060s. A faster transition would require not only a further acceleration in solar and wind deployment, but also the development of major grid storage capacity to replace natural gas. Although there is some grid battery storage today, it amounts to some 2 GWh (Source: PV Magazine), a tiny fraction of the amount that might be needed for a 100% renewable energy system. Further technical developments will be required, or perhaps storage will be combined with ultra-high voltage long distance transmission.

But the most static sector over a ten year period may well be heavy industry; sub-sectors such as cement, iron ore smelting and petrochemicals. While Sky sees some shift towards electricity, the change from 2020 to 2030 is modest. Carbon dioxide emissions remain unchanged at 400 million tonnes per annum over this period. Change is measured in decades rather than years. This is because of the time it takes to develop new industrial processes that don’t use fossil fuels for energy (e.g. hydrogen based iron ore smelting), retrofit exiting capacity and build the necessary infrastructure to support such change (e.g. hydrogen generation).

The next ten years is critical for a transition that meets the goals of the Paris Agreement and this was a feature of the House Resolution for a Green New Deal. Significant changes must be achieved to set the scene for net-zero emissions in the decades following. But to imagine wholesale energy system change in s decade is not realistic. There may well be narrow pockets of very deep change found in parts of the system, but complete change remains a fifty year project.

In Shell’s recently released Sky Scenario, around 1 billion electric passenger vehicles (EVs) could be on the roads as early as the 2040s. These 1 billion vehicles will each need a battery and while there are different battery chemistries available, it is likely that these batteries will need to include the vital element cobalt, a material that confers upon the battery good cycle ability and power output.

The new Tesla Model S has a Nickel-Cobalt-Aluminium Lithium Ion battery which contains just under 5 kg of cobalt, the lowest cobalt content of the various batteries that Tesla use.

While cobalt use per battery has fallen, with one manufacturer releasing information on the possible development of a cobalt free battery, some industry insiders believe that the Tesla Model 3 use of 10% cobalt in the battery cathode (8:1:1 Nickel:Cobalt:Manganese) is the minimum required for safety and battery longevity reasons.

If 8:1:1 were to be the dominant battery chemistry in the coming decades, an interesting dilemma emerges for automakers as they pursue electric vehicle development and rapid deployment. A look at global cobalt reserves, published recently in the BP Statistical Review of World Energy but drawing on data from the US and British Geological Survey, shows a current estimate of some 7 million tonnes, or 7 billion kilograms of cobalt. This is against current global production of 140 thousand tonnes, which has doubled over the last decade, giving a reserve to production ratio of 52 years.

The cumulative amount of cobalt (the stock) needed to be mined for passenger vehicle batteries will depend on the eventual number of cars in service (or batteries produced) and the amount of cobalt per battery. This stock is unrecoverable until cobalt is no longer used in batteries (or until cars transition again to some other propulsion mechanism), but it is reused repeatedly as older cars are scrapped, the cobalt recovered and recycled as new cars are built (the flow).

As the EV transition depicted in Sky gets going, the draw on cobalt increases and the stock builds. For example, by 2040 in Sky, 12.7 trillion vehicle kilometres are supplied by EVs, which could mean about 800 million to a billion vehicles on the basis of current usage patterns. At 4 to 5 kg each, that would require nearly 4 billion kilogrammes of cobalt, or more than half the global reserves. Before 2050 in Sky, the current global reserve of cobalt would be exceeded by EV deployment, without considering all the other demands for cobalt.

The above model assumes 100% recycle of cobalt as well, although this has little early impact in that recycle in 2040 will only come from production of EVs in the 2020s, which is still low compared to the potential 2040 stock. In any case, recycle is largely about annual flow, not stock. But an alternative model could emerge, which would see a much lower stock requirement for cobalt and therefore lessen the need to find alternatives, even with the same demand for passenger transport.

Autonomous vehicles offer the potential for vehicle sharing. If autonomous technology emerges rapidly, then the total number of cars in society can sharply decline under a vehicle sharing model, in that each car is used for a high percentage of the day, rather than parked awaiting the single use by its owner. While an individual car would likely have a much shorter life, say two to three years instead of fifteen, the stock requirement for materials such as cobalt would be much lower.

If by 2040 the number of EVs serving the above 12.7 trillion km demand is 100 million instead of 1 billion, then each vehicle would be driving 127,000 km per annum, leading perhaps to a two-year life after which there is either major refurbishment or even replacement. Annual production, or flow, of vehicles might remain largely unchanged, depending on the ratio of vehicles shared to vehicles owned and the life of a single vehicle under a high usage scenario. Whether the trend is towards refurbishment or replacement, the important materials such as cobalt are recycled and the total stock required by society is a fraction of the traditional ownership model. In a 100 million vehicle system, the required stock of cobalt could be as low as 500 million kilograms, just a fraction of current estimates of global reserves.

The above discussion introduces a new dimension into EV scenario thinking for auto manufacturers. The future might be dictated more by total vehicle stock considerations, in that manufacturers could encourage an alternative ownership model as the more cost-effective route forward to balance the demands on certain materials like cobalt. The alternative requires a continual search for different battery designs or seeking new deposits of hard-to-find minerals.

Note: Scenarios are not intended to be predictions of likely future events or outcomes and investors should not rely on them when making an investment decision with regard to Royal Dutch Shell plc securities. Please read the full cautionary note in http://www.shell.com/skyscenario.