Over recent weeks and months there has been considerable discussion in the USA and Canada on clean energy transition pathways, carbon pricing and the Paris Agreement. This has been catalysed by the IPCC 1.5° report, the arrival of new political figures on the scene and the prospect of elections in 2019 and beyond. As I discussed in my recent post on a new report that outlines a pathway for global transition consistent with 1.5°C, very steep emission reductions are called for in North America over the coming decade, as shown in the chart below. For the 1.5° case, a reduction of about 80% is proposed from 2015 to 2030.

Source: Achieving the Paris Climate Agreement Goals – Sven Teske (Editor)

But is such a rapid transition possible for an energy system as large as that found in the USA? This is similar to a pathway that has been proposed by those calling for a Green New Deal in the USA. But it is very different to that proposed by the Sky Scenario, released by Shell in 2018.

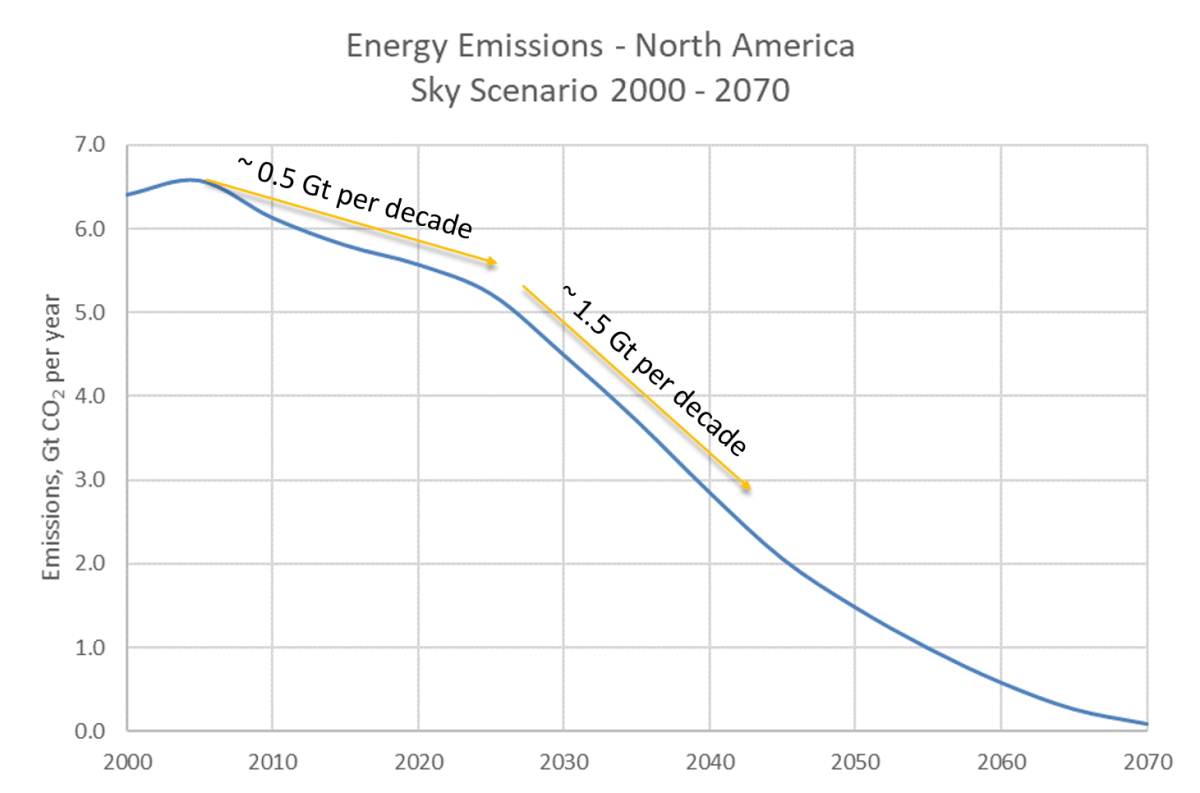

In Sky, to reach the goals of the Paris Agreement, global emissions need to peak in the 2020s and be falling by 2030, which happens in large part through an initial mobilization of effort throughout the 2020s. But emissions in the USA don’t get even close to an 80+% reduction in that time. North American emissions peaked around 2005 and are slowly falling, but in Sky the pace of change triples in the 2020s with a significant boost in effort, led by government policies such as carbon pricing and electric vehicle mandates and incentives. But by 2030, emissions have fallen by only 23% compared with 2015.

This would constitute a major shift in direction for the US economy. Five significant changes in the energy system in the decade to 2030 in Sky for North America are;

- Doubling of wind generation. This should be a relatively easy goal, but on the basis of current build rates it would not be met. Current US capacity is around 90 GW with a recent quarter seeing 0.6 GW added.

- A six-fold increase in solar generation. Current build rates would deliver about a third of the required capacity by 2030.

- Coal use down by a third.

- Natural gas demand plateaus and is the same in 2030 as it is in 2020.

- Electric vehicle (EV) sales boom and by 2030, 20% of all vehicle miles traveled are in electric vehicles.

To imagine even more than this is quite challenging. In the EV sector, sales in the USA in 2018 grew rapidly, but still only amounted to 2.1% of the total (Source: EVVolumes.com). A looming issue is the lack of EV models in the SUV / light truck category, although this should start to correct in 2020 with several expected. Nevertheless, this category size makes up a large portion of the US market and it may take some time for consumers to adopt electric versions of their favourite model. While an all EV sales line up might be possible by 2030, an all EV fleet isn’t. For a 100% EV fleet to occur in 2030, all new passenger vehicle sales need to be electric in the next year or two.

In the power generation sector, the multipliers given for wind and solar above, together with an unchanged role for nuclear, results in over half the power generation coming from non-fossil sources by 2030. In Sky, it isn’t until after 2040 before coal is phased out, but natural gas persists in the power mix until the 2060s. A faster transition would require not only a further acceleration in solar and wind deployment, but also the development of major grid storage capacity to replace natural gas. Although there is some grid battery storage today, it amounts to some 2 GWh (Source: PV Magazine), a tiny fraction of the amount that might be needed for a 100% renewable energy system. Further technical developments will be required, or perhaps storage will be combined with ultra-high voltage long distance transmission.

But the most static sector over a ten year period may well be heavy industry; sub-sectors such as cement, iron ore smelting and petrochemicals. While Sky sees some shift towards electricity, the change from 2020 to 2030 is modest. Carbon dioxide emissions remain unchanged at 400 million tonnes per annum over this period. Change is measured in decades rather than years. This is because of the time it takes to develop new industrial processes that don’t use fossil fuels for energy (e.g. hydrogen based iron ore smelting), retrofit exiting capacity and build the necessary infrastructure to support such change (e.g. hydrogen generation).

The next ten years is critical for a transition that meets the goals of the Paris Agreement and this was a feature of the House Resolution for a Green New Deal. Significant changes must be achieved to set the scene for net-zero emissions in the decades following. But to imagine wholesale energy system change in s decade is not realistic. There may well be narrow pockets of very deep change found in parts of the system, but complete change remains a fifty year project.